The Of Hsmb Advisory Llc

The Of Hsmb Advisory Llc

Blog Article

The Only Guide for Hsmb Advisory Llc

Table of ContentsThe Greatest Guide To Hsmb Advisory LlcThe Hsmb Advisory Llc DiariesThe Single Strategy To Use For Hsmb Advisory LlcTop Guidelines Of Hsmb Advisory LlcTop Guidelines Of Hsmb Advisory LlcHsmb Advisory Llc for BeginnersHsmb Advisory Llc Can Be Fun For Anyone

Under a level term policy the face amount of the plan remains the same for the whole duration. Frequently such policies are sold as mortgage defense with the amount of insurance coverage lowering as the balance of the home loan reduces.Generally, insurers have actually not can change premiums after the policy is marketed. Given that such policies may continue for many years, insurers need to make use of conventional mortality, interest and cost rate estimates in the costs estimation. Adjustable premium insurance, nonetheless, enables insurance firms to offer insurance policy at lower "current" costs based upon much less conventional assumptions with the right to change these costs in the future.

Some Ideas on Hsmb Advisory Llc You Should Know

The insurance coverage firm spends the excess costs dollars This kind of plan, which is occasionally called money worth life insurance policy, produces a cost savings aspect. Cash values are vital to an irreversible life insurance policy.

Often, there is no relationship between the size of the cash value and the costs paid. It is the cash worth of the policy that can be accessed while the insurance policy holder lives. The Commissioners 1980 Requirement Ordinary Mortality (CSO) is the current table made use of in computing minimal nonforfeiture worths and plan gets for common life insurance policy policies.

The Hsmb Advisory Llc Statements

There are two basic categories of irreversible insurance coverage, standard and interest-sensitive, each with a number of variations. Typical whole life policies are based upon long-lasting price quotes of cost, interest and death.

If these quotes transform in later years, the company will readjust the premium accordingly however never ever over the maximum guaranteed costs stated in the policy (Life Insurance). An economatic entire life policy attends to a fundamental quantity of taking part whole life insurance policy with an additional extra insurance coverage offered via using returns

Due to the fact that the premiums are paid over a much shorter period of time, the premium repayments will certainly be more than under the whole life strategy. Single premium whole life is restricted settlement life where one large premium settlement is made. The plan is fully compensated and no more costs are called for.

The Best Strategy To Use For Hsmb Advisory Llc

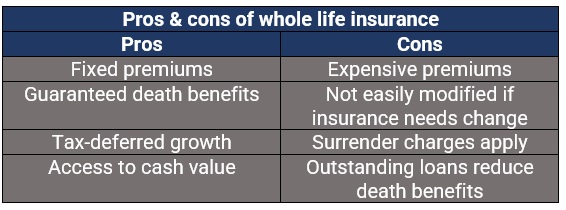

Because a substantial repayment is included, it should be deemed an investment-oriented item. Rate of interest in single premium life insurance official source coverage is largely due to the tax-deferred therapy of the accumulation of its money worths. Taxes will be incurred on the gain, nevertheless, when you give up the plan. You might borrow on the cash worth of the policy, however bear in mind that you may sustain a substantial tax expense when you surrender, even if you have actually obtained out all the money value.

The advantage is that enhancements in rates of interest will certainly be mirrored faster in interest delicate insurance coverage than in typical; the negative aspect, of training course, is that decreases in rates of interest will certainly likewise be felt faster in rate of interest delicate entire life. https://lwccareers.lindsey.edu/profiles/4506780-hunter-black. Health Insurance St Petersburg, FL. There are four basic interest sensitive whole life plans: The global life policy is actually even more than passion sensitive as it is developed to mirror the insurer's existing death and expense in addition to passion earnings instead of historical prices

How Hsmb Advisory Llc can Save You Time, Stress, and Money.

The business credit histories your premiums to the cash value account. Occasionally the firm deducts from the money worth account its costs and the cost of insurance defense, usually called the death reduction fee. The balance of the cash money worth account gathers at the rate of interest credited. The business assures a minimal rate of interest rate and an optimum death fee.

Existing assumptions are essential to interest sensitive items such as Universal Life. Universal life is likewise the most adaptable of all the numerous kinds of plans.

Hsmb Advisory Llc Fundamentals Explained

It is necessary that these presumptions be sensible since if they are not, you might have to pay even more to maintain the plan from decreasing or lapsing. On the other hand, if your experience is much better after that the presumptions, than you may be able in the future to skip a premium, to pay much less, or to have actually the strategy paid up at an early date.

On the various other hand, if you pay more, and your assumptions are practical, it is possible to compensate the plan at an early date. If you give up a global life plan you may receive much less than the cash money worth account as a result of abandonment costs which can be of 2 kinds.

More About Hsmb Advisory Llc

Report this page